How a Foreigner can receive his Philippine Land Inheritance (Updated for 2018 TRAIN Law)

Yes, a foreigner can inherit Philippine assets (with some restrictions).

If you are a foreign heir to a Philippine land inheritance, this post is particularly for you.

This post answers common questions as to whether you can inherit, how much you can inherit and the process and payments to put the title in another person’s name (this is needed when you sell the property).

It also goes through a common real life example of a person who died without a will, but left behind:

- a family home;

- a bank account;

- unpaid real estate taxes.

A few notes:

Be prepared to work with your co-heirs (otherwise the process becomes considerably more difficult) and to pay taxes due on the estate.

Also, be prepared to go to a number of government offices in person to coordinate. Most things still cannot be done through the phone or the internet.

Contents

- Can you inherit Philippine Land as a foreigner?

- How much can you inherit as a foreigner?

- How do you transfer the Philippine property to your name?

- Will I have to pay to settle the estate?

- How much will I have to pay to settle the estate?

- How much would I pay to settle the estate if the only assets are the family home and a bank account?

- Summary

Can you inherit Philippine Land as a foreigner?

Yes, you can inherit land in the Philippines if the person you inherited from died without a will.

However, you cannot inherit Philippine land if the person you inherited from died with a will.

The law is very firm on this.

In fact, inheriting intestate (inheriting when there is no will) is the only way that a foreigner can own land in the Philippines.

A foreigner can inherit land if the deceased had no will.

A foreigner cannot ordinarily own Philippine land at all, with the exception of former Filipino citizens who can purchase restricted quantities of land.

This post deals specifically with the case of a foreigner who inherited Philippine land from a Filipino when the deceased Filipino died without a will.

How much can you inherit as a foreigner?

You inherit a set portion of an estate when you inherit without a will.

The amount you inherit is set down by Philippine law.

The amount cannot be changed unless the other heirs agree.

Your portion will depend on who else are heirs according to the law.

Usually, an estate is divided among relatives. Spouses and children are prioritized.

If your father and your mother had children, grandparents, parents and siblings do not usually inherit. If your parents had no children, then they stand to inherit.

There is an entire table on this and it is quite detailed.

How do you transfer the Philippine property to your name?

Now that you know you are an heir, your number one question is likely how you can transfer the title of these properties to yourself or an interested buyer.

Many new owners will want the title in their name since this ensures that their ownership is not challenged. If the title is in another’s name, that person or his heirs can claim it.

You can only do this through a process called “settling the estate”.

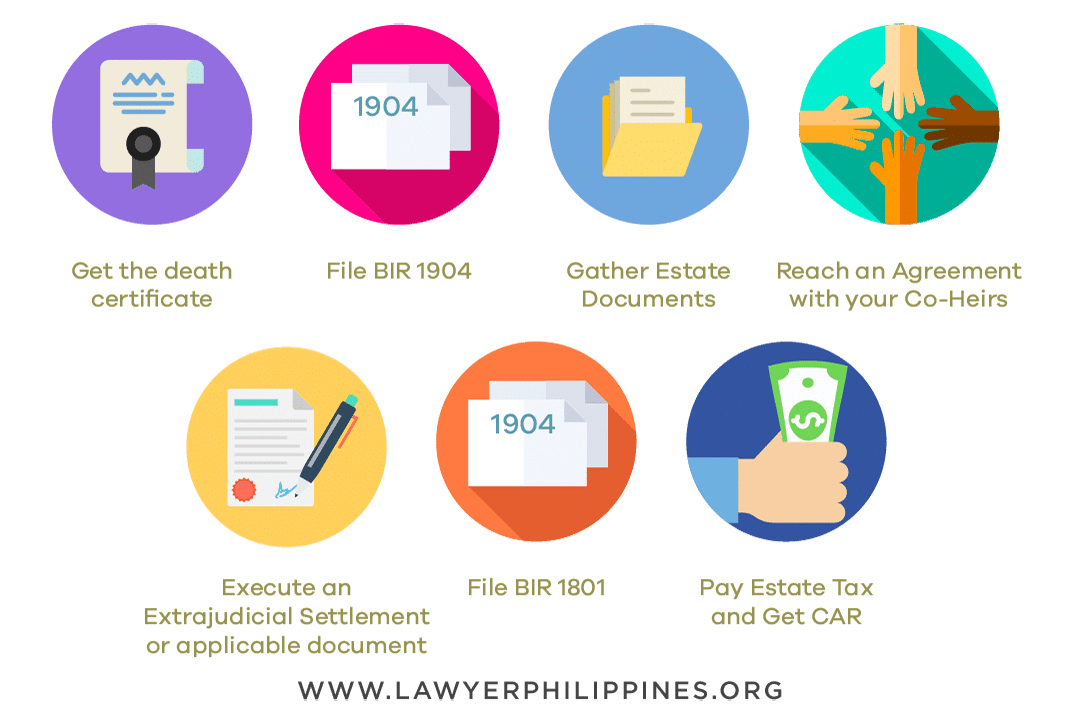

There are 7 steps to settling an estate.

Settling the estate means paying estate tax to the BIR, any unpaid real estate taxes, and debts, and then agreeing with your co-heirs on the estate details. Only then can you transfer property to another.

It has several steps:

- Get the death certificate

- File BIR 1904

- Gather Estate Documents

- Reach an Agreement with your Co-Heirs

- Execute an Extrajudicial Settlement or applicable document

- File BIR 1801

- Pay Estate Tax and Get CAR

This is a pretty involved process, so you’ve really got to commit to spending time and money on it.

You’ll need someone to physically visit all the government offices.

Some common problems you may face if you are living abroad are:

- You may need to physically visit Philippine government offices to complete the process

- You have to agree with your co-heirs

- You have to have the money to pay for the debts and unpaid taxes

- You have to have any of the documents

You’ve really got to work with your co-heirs who are in the Philippines.

They will likely be able to find the documents and visit the government offices. Together, you can also decide how you are going to pay the estate’s obligations.

You’ve got to pay these obligations so that you can receive the BIR’s clearance.

This clearance is called the Certificate Authorizing Registration and will now allow you to sell or transfer the property.

Will I have to pay to settle the estate?

You will have to pay before being able to sell or transfer the property.

Why?

Well, the BIR will not allow you to transfer property to another person without you paying all previous debts or taxes which is called “settling the estate”. The Registry of Deeds also needs this BIR clearance to transfer to a new owner.

You might be tempted to postpone settling the estate.

Don’t!

It will end up costing you and your co-heirs more money.

Settling an estate can be a long process.

The BIR only gives you 1 year after a death to settle the estate. Afterwards, it will start to charge you penalties:

- 25% surcharge on the tax due if not paid on time

- 20% interest rate on the tax due

If it goes on long enough, the tax due can be too much to handle and can be more than your inheritance.

How much will I have to pay to settle the estate?

One of the first steps you’ll have to accomplish is to figure out what the estate owns and owes.

What the estate owns could be:

- Family home and other real estate

- Stocks and Bonds

- Vehicles and other Assets

What the estate owes could be:

- Debts

- Unpaid real estate taxes

- Other obligations

When you calculate the estate, you will need all the documents that show ownership.

At this point, you should also call an accountant or an estate lawyer.

Things can get complicated and they’d be able to figure out legal ways to lower your obligations or if foreign tax treaties apply to you.

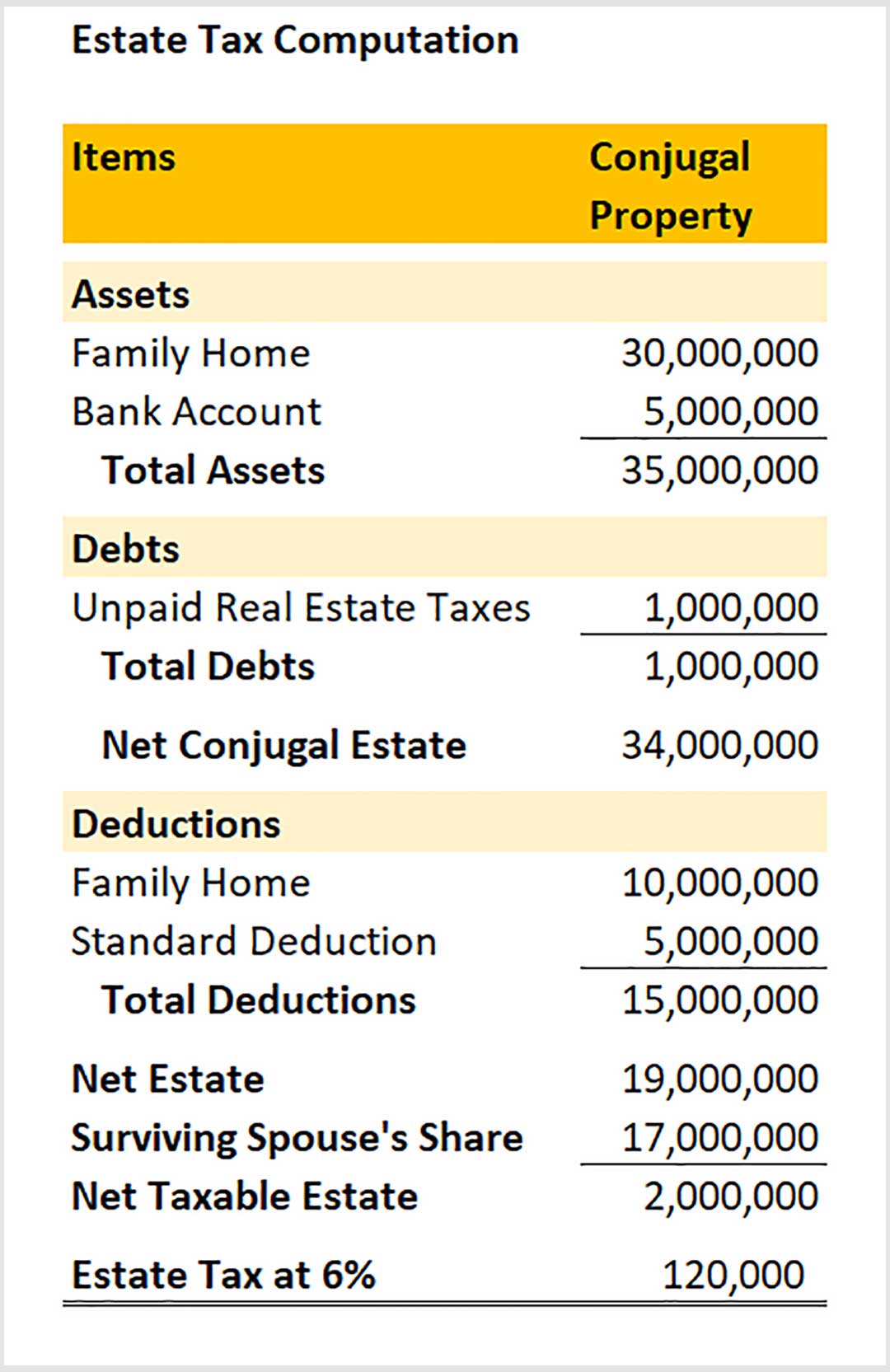

How much would I pay to settle the estate if the only assets are the family home and a bank account?

A very common scenario is when the only asset of the estate is the family home.

You, your mother and your brother inherited equal shares in your father’s estate. Your mother and father’s property marriage regime is that of absolute community.

Your father’s estate is composed of a family home in Mandaluyong, a bank account and unpaid real estate taxes.

Let’s take a look at this case with the hard numbers:

Now, that’s the answer.

But how do you get there?

Below, you’ll find the most practical approach to calculating what to pay.

(Hint: Hire an accountant!) 🙂 But joking aside, you really need someone well-versed in tax to be able to help you calculate the amount you will need to pay.

You will most certainly need to get all the documents related to the property and then start accounting what the estate owns and owes.

This will help you figure out exactly how much is needed.

Professionals are often needed to settle an estate because it can get complicated.

A good accountant and lawyer is even more important when the estate is complicated.

They might know of tax treaties to help you avoid being taxed in the Philippines and in your country.

They might know of tax exemptions to lower your estate taxes.

The more information you give them, the more they will be able to save you money. It is important that you give them as much documentation as you can.

Summary

If you want to sell or transfer property to your name, you will have to get clearance called a Certificate Authorizing Registration from the BIR.

You cannot get this clearance without paying estate taxes and unpaid realty taxes. This is called settling the estate.

Settling the estate with the BIR involves:

- Agreeing with your co-heirs

- Gathering essential documents

- Finding the money to pay estate taxes and other obligations.

Settling the estate can be complicated and a good accountant and lawyer should be able to advice you on how to best save on estate taxes.

After you settle the estate, the property can then be successfully sold or transferred after registering with the Registry of Deeds.

0 Comments