How to Set Up a Representative Office Philippines: Complete Guide for Businesses

Looking to cut costs and offshore back-office work?

A Representative Office in the Philippines might be your best option.

A representative office in the Philippines acts as an extension of a foreign company, providing an opportunity to offshore non-revenue generating activities, such as customer support and quality control so as to reduce costs.

A foreign representative office allows 100% foreign ownership and control. It also has a simplified governance structure that is easier to manage than a domestic corporation.

For these reasons, it is the go-to corporate structure for those looking to take advantage of the Philippines’ well educated and cheaper workforce.

This article covers everything you need to know about setting up a Representative Office Philippines from requirements, benefits, restriction, and step-by-step registration.

Contents

- Representative Office Philippines: What is it?

- Representative Office Philippines: Comparative Analysis of Business Structures

- Representative Office Philippines: Control, Liability, Nature of Business

- Representative Office Philippines: Capitalization

- Representative Office Philippines: Address

- Representative Office Philippines: Resident Agent

- SEC Requirements for Representative Office Philippines

- Representative Office Philippines: SEC Registration Process and Other Steps

- What are the Common Challenges to setting up a Representative Office in the Philippines?

- Frequently Asked Questions

Representative Office Philippines: What is it?

What is Representative office in the Philippines?

A Representative Office Philippines is a very popular structure for foreign entities looking to do business in the country as it allows 100% foreign ownership and control.

Here is the list of important features of a Representative Office:

- Extension of the foreign company

- It may perform services such as quality control, information dissemination, customer service and other business processes

- Liability is shared with the parent company

- Instead of a Board, a Representative Agent is needed who must be a resident of the Philippines

- A non-revenue generating entity that does not derive income from any of the services it offers in the Philippines.

- 100% foreign ownership & control

- Inward remittance of USD 30,000 annually to fund the Representative Office in the Philippines as it is fully subsidized by the head office

- Representative Office Taxation is easier to manage as there is no income tax to pay as it does not generate any income and correspondingly no VAT on that Withholding taxes are applicable

So, a Representative Office Philippines is generally used as a low cost back office for administrative tasks such as accounting and accounting. It is also often used to handle customer service and quality assurance tasks.

On the other hand, a Representative office cannot generate income as it is a non-revenue generating entity.

To better understand, here is an example:

A foreign IT firm sets up a Representative Office in the Philippines, specifically in Manila.

It is allowed to:

- Marketing & Promotion: Showcase software products to potential clients or partners.

- Training & Support: Conduct workshops, seminars, or onboarding sessions for users or resellers.

- Quality Control: Ensure standards are met for software distributed abroad.

- Information Dissemination: Share product updates, technical specs, or company news.

It cannot do the following:

- Local Sales: Cannot sell software licenses or services directly in the Philippines.

I’ll discuss each in more detail below. For additional information or for a personal assessment, please contact us to set up a consultation with a corporate lawyer in the Philippines.

Representative Office Philippines: Comparative Analysis of Business Structures

Why Choose a Representative Office?

A Representative Office Philippines is a popular choice but is often considered in conjunction with a Branch Office and a Domestic Corporation.

To compare them quickly against each other, I’ve put together a table of comparison.

Choose the business structure that aligns with your investment strategy in the Philippines.

As you can see, there are several benefits to establishing a Representative Office Philippines.

- Cost Efficiency: Establishing a representative office is typically more economical than setting up a branch, making it an appealing option for companies looking to offshore their cost centers with minimal financial commitment. A non-revenue generating entity requires USD 30,000 to establish.

- Simplified Taxation: Since representative offices do not generate income, they are exempt from income tax and sales taxes, which simplifies financial management for foreign companies.

- Simplied Governance: Instead of a board, a representative agent is needed. A representative agent must be a resident of Philippines and can be a local, a foreigner or another entity.

- 100% Foreign Ownership: A representative office is 100% owned and controlled by its foreign parent.

- Market exploration: establish a corporate footprint to first understand the market.

- Build a brand presence: A representative office allows you to introduce yourself to the Philippine market before further investment.

Representative Office Philippines: Control, Liability, Nature of Business

Unlike a branch office that can sell to the Philippine market, a representative office acts as a cost center.

A foreign representative office is an extension of a parent incorporated abroad.

Due to the fact that it is an extension, a Representative Office has the following traits:

- It shares liability with its parent

- It has the same type of business as its parent

- It is fully owned by its parent

As a Representative Office is an extension of its parent, they are considered the same entity.

Because of that, liability is shared.

This is often a concern, and so many people may opt instead to form a domestic corporation as that does not share liability with the parent.

It’s a business structure that serves as an office extension of a foreign company that acts as administrative support or liaison office.

If the purpose of the parent is to sell software, then the Representative Office can engage in non-revenue generating activities that support the selling of software. These activities may be things such as the following:

- Quality control

- Customer support

- Accounting

This doesn’t cover everything, but it is a good example of the processes that a Representative Office Philippines can do in support of the same business line as its parent.

If the purpose of the Philippine presence is to form an entirely new business, then the domestic corporation should be considered instead.

Generally, a Representative Office in the Philippines is set up when a foreign entity wants to offshore administrative or support functions to control costs.

Representative Office Philippines: Capitalization

USD 30,000 is the capitalization needed for a Representative Office in the Philippines.

A Representative Office Philippines does not earn income.

Because of that, it’s parent must fully subsidize its operations.

The setup cost is a minimum capital requirement of $30,000 USD.

This capital is remitted inward in the Philippines initially to start the operations.

Then, USD 30,000 must be remitted annually to sustain the local organization.

As Representative Office is a non-revenue generating entity, several taxes would not apply such as sales and income taxes.

However, it must still register with the BIR for compliance purposes and for other taxes that it is eligible for.

Representative Office Philippines: Address

It is also important to use an office address not a condo or an apartment to avoid future conflicts with licenses and permits.

During the process of company formation in the Philippines, an address will be needed.

It is possible to use a temporary address.

However, it is advisable to make sure that the address is in the same Bureau of Internal Revenue District Office (BIR RDO) and the same local government unit.

It is possible to change a corporate address – however, it is quite a lot of work.

The Philippines Representative Office must essentially be closed at the local government units and the BIR RDO.

Then, they must be opened at the BIR RDO and the local government unit that has jurisdiction over the new corporate address – with the added fact that the company will likely go through a BIR audit before closure.

Transfer of business address could take up to 6 months or more than a year depending on the result of the BIR audit.

This BIR audit takes a while to complete.

And if it sounds like closing and reopening a representative office registration sounds like more work than the initial process of company formation in the Philippines, that’s because it is.

A company we work with transferred offices and the transfer process has taken more than a year.

Contact us for a consultation with a corporate lawyer in the Philippines from our staff if you need help or have additional concerns.

Representative Office Philippines: Resident Agent

The appointment of a resident agent is highly recommended and must be authorized by a resolution of the Board of directors and an executed agreement of the Board of Directors of the foreign entity.

A Resident Agent is required during company formation for a Representative Office.

A Resident Agent is the person that the SEC and other government agencies such as the court will serve notices to if there is a need.

A Resident Agent may also sign such things as the SSS enrollment form R1, as one of the post-SEC requirements for Representative Office Registration.

Resident Agent Guidelines:

- Must be a resident of the Philippines

- Can be a local, a foreigner or a domestic corporation

- A domestic corporation must be a company certified to be in good standing with the SEC

Check out our post on Resident Agents in the Philippines or get in touch with a corporate lawyer in the Philippines.

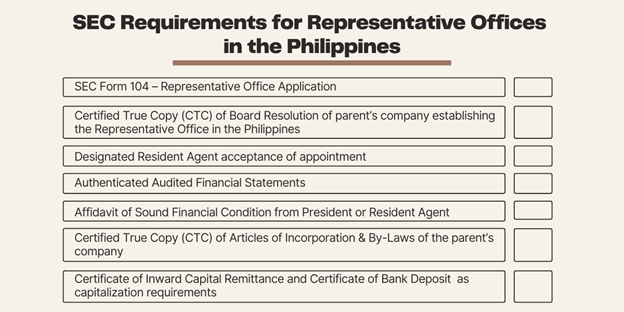

SEC Requirements for Representative Office Philippines

The first stage of company registration is SEC licensing, after which the company must also process other requirements at the local government level.

SEC Requirements for Representative Offices in the Philippines are below

(you can also download it here):

- SEC Form 104 – Representative Office Application

- Name Verification Slip

- Certified True Copy (CTC) of Board Resolution of parent’s company establishing the Representative Office in the Philippines

- Designated Resident Agent acceptance of appointment

- Authenticated Audited Financial Statements have several guidelines for how they must be prepared. The financial ratio must be 1 for Total assets/Total Liabilities

- Affidavit of Sound Financial Condition from President or Resident Agent

- Certified True Copy (CTC) of Articles of Incorporation & By-Laws of the parent’s company

- Certificate of Inward Capital Remittance and Certificate of Bank Deposit of US$30,000.00 as capitalization requirements

Apostille Philippines has a lot of legwork but once you learn the process you can get it easier.

SEC Requirements for Representative Offices do look easy.

However, companies usually encounter delays in the authentication of the documents because it is quite cumbersome.

Authentication can be done either through the authentication process itself or through apostille.

Authentication is done when a country is not part of the Hague Convention.

It requires consularization at the PH embassy.

Apostille is done when a country is part of the Hague Convention and is different for each country. Still, there are often several steps.

Additionally, preparing the Audited Financial Statement (AFS) as per the guidelines can also take a long time.

SEC rules require a foreign businesses to file annual reports and submit authenticated audited financial statements if AFS exceeds one year.

The guidelines for SEC requirements for Representative Office’s Financial Statements have revised a few years ago, but it can still take a lot of work.

Here are the guidelines:

- For countries where Audited Financial Statements are required, the Authenticated AFS for the previous year audited by an independent CPA is required.

- For countries where Audited Financial Statements are required and the Audited Financial Statements are more than a year old, the latest Authenticated Audited Financial Statements can be submitted along with Authenticated Unaudited Financial Statements not exceeding one year can be accepted.

- For countries where Audited Financial Statements are not required, authenticated unaudited financial statements not later than a year are required. In addition, an authenticated Certification from the company’s legal counsel stating that audited financial statements are not required and stating the supporting law.

Representative Office Philippines: SEC Registration Process and Other Steps

You can get the representative office build-up assistance by contacting a corporate lawyer in the Philippines.

The establishment of a representative office necessitates adherence to SEC regulations.

In terms of incorporation, documentation such as financial statements and proof of inward remittance are required.

After incorporation, there are several reporting requirements that must be adhered to as well.

Representative Office Philippines: Step-by-Step Process

The process of setting up a Representative Office can help reduce costs, as it is a non-revenue generating entity in the Philippines that helps provide low-cost support functions to its parent.

Step 1: Gather the SEC requirements

- You will need the documents I stated in the above section, which include SPAs, director information, board resolutions and Audited Financial Statements.

- Appoint a Resident Agent and present an acceptance of appointment unless he signed the application form

- Ensure you have an address

Step 2: Open a Bank Account & Deposit Capital

- Fund the business and get a Certificate of Inward Remittance and a Bank Certificate of Deposit

- Minimum Capital Requirement: $30,000 USD Remittance from Parent Company.

Step 3: Register at the SEC

- Upload the requirements

- Pay the SEC fees which is 1/10% of 1% of the actual inward remittance in Philippine peso, but it should not be less than Php 2,000

- Address SEC concerns, if applicable

- Pick up the Certificate of Registration

Step 4: Register with the Bureau of Internal Revenue (BIR)

- Get a Taxpayer Identification Number (TIN).

Step 5: Obtain Local Permits

- Secure Barangay Clearance for office location.

- Register with the Local Government Unit (LGU) for a Mayor’s Permit.

What are the Common Challenges to setting up a Representative Office in the Philippines?

Setting up a Representative Office in the Philippines allows a global company to build a brand presence and support activities locally, however, it is essential to understand the potential obstacles foreign companies face and determine how to address them.

Challenge 1: Misunderstanding Representative Limitations

Foreign investors may set up a Representative office without in-depth understanding about the limitations related to the business structure.

Solution: Work with a local legal consultant to ensure compliance.

Challenge 2: Lengthy Approval Process

Setting up a Representative Office in the Philippines can be time-consuming, as agencies carefully review foreign documents that often require notarization or authentication.

The process also involves coordinating with several government bodies with their own timeline, while strict compliance rules add further complexity to approval.

Solution: Prepare complete documentation before submission.

Challenge 3: Foreign Exchange Compliance

All operating funds of Representative office Philippines must come from the parent company abroad and must be properly documented through inward remittance. This requires strict coordination with authorized banks and the BSP, making the process time-consuming and heavily regulated.

Solution: Use authorized remittance channels for capital transfer.

A Representative Office is a cost-effective way to establish a presence in the Philippines without financial risks. However, it comes with operational limitations.

Thinking of setting up an RO?

Consult our legal team to streamline your registration process and ensure compliance with Philippine regulations.

For more details on business structures, check out our guide on Branch Offices in the Philippines.

Frequently Asked Questions

Below are the Frequently asked questions about representative office Philippines

1. What activities can a representative office perform?

A representative office is permitted to conduct activities such as marketing, quality control, and customer service, but it cannot generate income.

2. What are the costs associated with setting up a representative office?

The primary financial obligation involves an annual remittance of USD 30,000 from the parent company to cover the operational expenses of the office.

3. What is the liability of a Philippine representative office?

The liability of a Philippine representative office is shared with its parent entity.

4. Can a Philippine representative office be 100% foreign owned?

Yes, a Philippine representative office can be 100% foreign owned.

5. What is the difference of Branch Office vs Representative office?

A Branch Office can derive revenue from the Philippines while a Representative Office cannot. Additionally, a Branch Office’s minimum capitalization is USD 200,000 vs a Representative Office’s minimum capitalization of USD 30,000.

{kind=link}

Hi a foreign company wishes to establish an office in the Philippines working for designs and planning support for the parent company but the number of employees might reach up to 50 people. They dont intend to generate income in the Philippines. What is the best structure. A representative or Branch Office? What is the time frame for SEC registration

Since your company will only provide design and planning support and won’t generate income locally, a Representative Office is the appropriate legal structure. However, this also need further legal consideration under Philippines law so I suggest seeking corporate lawyers that will help you establish the appropriate legal business structure. You may email us at admin@lawyerphilippines.org or book a consultation with us. Thank you!

Is there a maximum limit for the number of employees for Rep Office?

There is no statutory maximum limit on the total number of employees can hire.